This leads to the need for maintaining all cash transactions in one place for the business and necessitates the use of a cash book. In contrast to utilising a cash book template, companies today prefer maintaining records with excel sheets or accounting software. Among the different types of maintaining a petty cash book or a full-fledged one, the three types are as discussed below. An original entry in a cash book is a record of a financial transaction. The bank cash book is a type of cash book that is used to track the transactions between a business and its bank.

FAQs on Cash Books

A cash book includes receipts and payments of cash, credit sales, and more. It shows the date of a transaction, the name of the customer (if applicable), account to be debited (positive amount) or credited (negative amount). The balance is placed in the ledger as a cash account by the end of the day. Cash books are crucial since they are used to document all cash receipts and payments.

What Are the Different Types of Cheques?

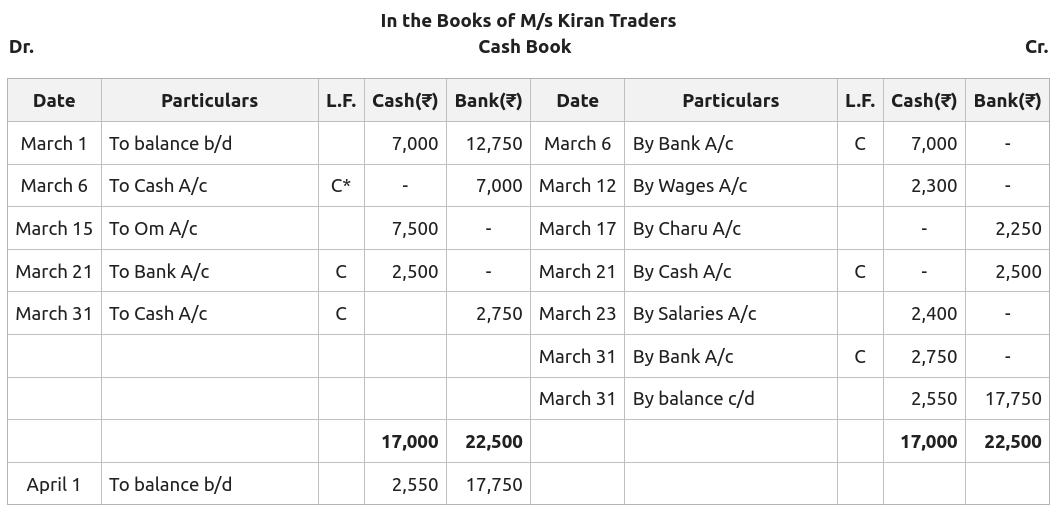

The difference is that here we also record banking transactions i.e., the transactions in which bank is also involved. Bank facilitates a business enterprise to open current account in which the business enterprise can withdraw amount in excess of what is available in the current account. The triple column cash book is a compact form of cash book in which all the three columns, i.e., cash, bank and discount, are included.

Filling the Cheque

In addition to serving as an important accounting record, it helps companies in keeping track of their financial position at all times. It also provides updated and relevant data while formulating budgets, making forecasts, and allocating resources, thus, ensuring efficient financial management. The main differences between a cash book and a pass book are how they track payments in cash and receipts, and who tracks them. A cash book format will track all of the money that is deposited and withdrawn from the account.

Petty cash book is based on the division of labour and works on imprest system; hence, it reduces the work and labour of main cashier. In the ‘L.F.’ (Ledger Folio) column, the folio (page number) of the respective ledger, where the posting of the transaction is made, shall be recorded. Here we detail about the three types of cash book, i.e., (1) Simple Cash Book, (2) Two Column Cash Book, and (3) Petty Cash Book. Unlike other journal registers like sales and purchases, the cash book is in “T form”, just like a ledger. The transaction that took place first will be entered first in the cash book.

Posting Petty Cash Book to Ledger

If a payment is made by cheque, it will be recorded on the credit side in the bank column. The only exception is that a column is added in a three column cash book to account how to do a journal entry for purchases on a notes payable chron com for bank-related transactions. It is customary for businesses to allow discounts for early payments. For example, if cash is paid early, creditors may receive a discount.

- This person holds the bank account from which the funds will be drawn.

- A cash book contains receipts and payments of cash, credit sales, etc.

- When money is received, an original receipt is given to the payer and the payee retains a copy.

- At the end of the period, we balance both columns and transfer the closing balances.

- The difference is that here we also record banking transactions i.e., the transactions in which bank is also involved.

A folio number is a unique number assigned to a specific ledger account mentioned in the description column for easy reference and cross-verification. To illustrate, for a company receiving cash payment for sales, entries will be made both in the sales ledger and the cash book. A cash book is an important tool for businesses to help track their finances. They allow businesses to keep track of payments and receipts in a detailed way. This can be used to make important decisions about the future of the business.

The book in which these small payments are recorded is known as the petty cash book. The funds used for small payments are known as petty cash, and the person responsible for making and recording these payments is the petty cashier. A petty cash book also refers to the book in which small payments are recorded, which are not convenient to record in the main cash book.

This legal standing adds an extra layer of trust in transactions. The cheque drawer is the individual who signs and authorises the cheque. This person holds the bank account from which the funds will be drawn. By signing the cheque, the drawer confirms that they wish to pay the payee. A banker’s cheque is issued by the bank on behalf of its customer, guaranteeing payment. This makes it ideal for large or important transactions, as the bank itself backs the payment, ensuring its security.

For every entry recorded in the cash book, there must be a proper voucher. The right-hand side is the debit side which records all the receipts. The left-hand side is the credit side which records all the payment transactions.