Implementing lean manufacturing techniques, investing in modern equipment, and providing ongoing training for employees can enhance production efficiency and reduce material waste. Additionally, regular audits of the production process can identify areas for improvement and help maintain optimal material usage. Direct Material Price Variance is the difference between the actual cost of direct material and the standard cost of quantity purchased or consumed. Direct materials price variance account is a contra account that is debited to record the difference between the standard price and actual price of purchase.

Material Price Variance Calculator

By delving into the specifics of variances, companies can uncover inefficiencies and make informed decisions to optimize their operations. The first step in this analysis is to regularly review variance reports, which provide a snapshot of how actual costs compare to standard costs. These reports should be detailed and timely, allowing managers to quickly identify and address any discrepancies. Understanding the factors that influence direct material variance is essential for businesses aiming to maintain control over their production costs.

Formula:

For example, if a material price variance is detected, managers should examine market conditions, supplier performance, and procurement strategies to pinpoint the cause. Similarly, if a material quantity variance is found, a thorough review of the production process, employee performance, and equipment efficiency is necessary. This investigative approach ensures that corrective actions are targeted and effective. Supplier performance also plays a crucial role in direct material variance. Reliable suppliers who consistently deliver quality materials at agreed-upon prices help maintain stable production costs. Conversely, issues such as late deliveries, substandard materials, or unexpected price hikes can lead to variances.

What is your current financial priority?

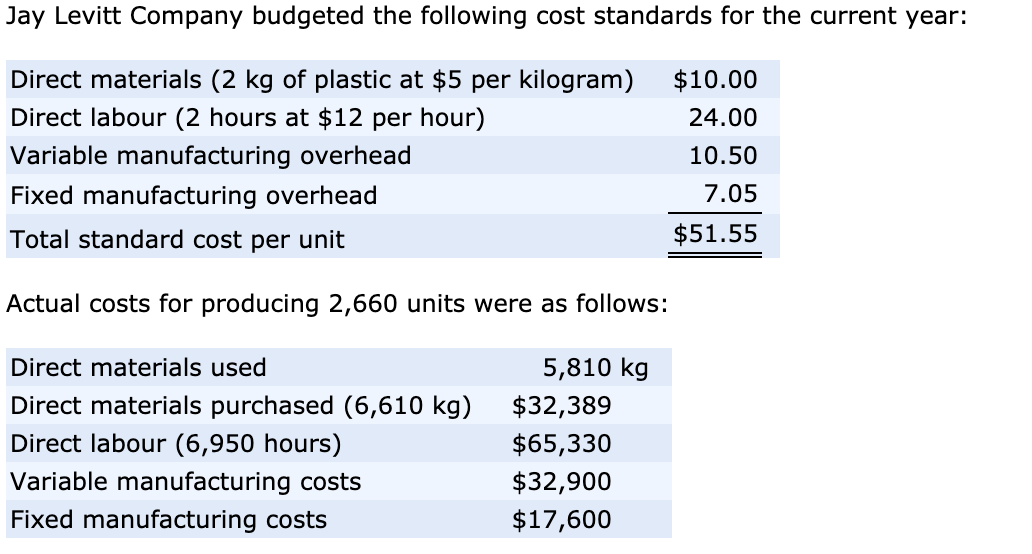

In most other cases, the purchasing manager is considered to be responsible. Direct material price variance measures how much more or less you spent on materials compared to your plan. Your aim should be a thorough and error-free record of every raw material that goes into your products. Using the materials-related information given below, calculate the material variances for XYZ company for the month of October. Managers can better address this situation if they have a breakdown of the variances between quantity and price. Specifically, knowing the amount and direction of the difference for each can help them take targeted measures forimprovement.

It’s important to note that direct material variance can be broken down into more specific components, such as price and quantity variances. However, the initial calculation provides a broad overview that can guide more subject to change detailed analysis. By regularly monitoring these variances, businesses can quickly identify trends or anomalies that may indicate underlying issues, such as supplier problems or inefficiencies in the production process.

If the actual purchase price is higher than the standard price, we say that the direct material price variance is adverse or unfavorable. This is because the purchase of raw materials during the period would have cost the business more than what was allowed in the budget. The difference column shows that 200 fewer pounds were used than expected (favorable). It also shows that the actual price per pound was $0.30 higher than standard cost (unfavorable). The direct materials used in production cost more than was anticipated, which is an unfavorable outcome.

- Effective management of direct material variance can lead to significant savings and better resource allocation.

- Maybe they switched to a new supplier or had to order materials in a rush and paid more.

- Learn how to calculate, analyze, and apply direct material variance for effective cost control and improved financial performance.

- Additionally, regular audits of the production process can identify areas for improvement and help maintain optimal material usage.

- Therefore, the purchase cost of the entire quantity must be compared with the standard cost of the actual quantity.

It’s not just about knowing the number of units but understanding their role in cost variance calculation too. Accurate tracking ensures that any price difference evaluation reflects true production costs. Effective management of direct material variance can lead to significant savings and better resource allocation.

Material price variance analysis helps management identify areas for cost improvement, assess supplier performance, and evaluate the effectiveness of cost control measures. However, it’s essential to consider other factors that may influence costs, such as changes in material quality or production processes, when interpreting variance results. Materials price variance (or direct materials price variance) is the part of materials cost variance that is attributable to the difference between the actual price paid and the standard price specified for direct materials. The direct materials price variance of Hampton Appliance Company is unfavorable for the month of January. This is because the actual price paid to buy 5,000 units of direct material exceeds the standard price.

Direct material price variance (DM Price Variance) is defined as the difference between the expected and actual cost incurred on purchasing direct materials. It evaluates the extent to which the standard price has been over or under applied to different units of purchase. With our direct material price variance calculator, we aim to help you assess the difference between the actual cost of direct materials and the standard cost. To understand more on this topic, check out our unit price calculator and cost of goods sold calculator. Direct materials quantity variance is a part of the overall materials cost variance that occurs due to the difference between the actual quantity of direct materials used and the standard quantity allowed for the output.